Vea también

04.03.2026 01:23 PM

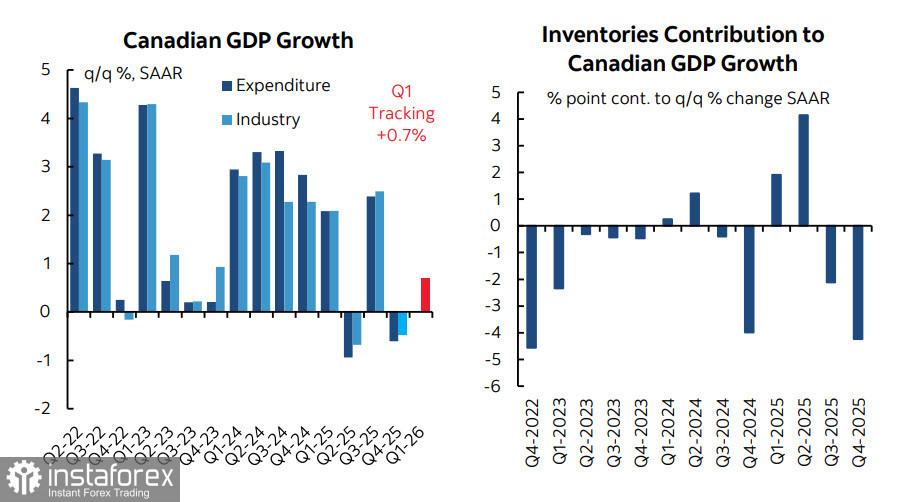

04.03.2026 01:23 PMCanada's economy contracted by 0.6% in the fourth quarter, below the Bank of Canada's forecast of flat growth and the consensus expectation of a milder 0.2% decline versus Q3. For the year 2025, Canada's economy expanded by 1.7%, down from 2.0% in 2024. Preliminary expectations for Q1 of the current year are for +0.7%, but such forecasts should be treated with caution given the high level of global uncertainty.

The details are mixed. For example, the decline in output was driven solely by an inventory drawdown, while core domestic demand performed much better, rising 2.4% quarter-on-quarter. Investment in housing fell noticeably, but government investment increased and the trade balance improved—a surprising outcome given higher tariffs from a major importer, which would normally be expected to dent export volumes.

The report is weaker than the Bank of Canada's January forecasts and reinforces a bearish tilt on the rate outlook. Signs of the labor market slack and a gradual easing of inflation persist. Taken together, these factors suggest the Bank of Canada will keep the policy rate at 2.25% at the next meeting on 18 March, although new labor market and inflation data due on 13 and 16 March mean the rate projection must be viewed as provisional.

The war in the Middle East is also a major uncertainty. If it drags on — and it is too early to assume otherwise — a spike in inflation driven by sharply higher energy prices is inevitable. Gasoline prices in the United Kingdom are already up by more than 70%, and Japan's Nikkei has tumbled sharply since Japan previously sourced up to 70% of its oil and petroleum products via the Strait of Hormuz. A global inflation surge, therefore, looks increasingly likely.

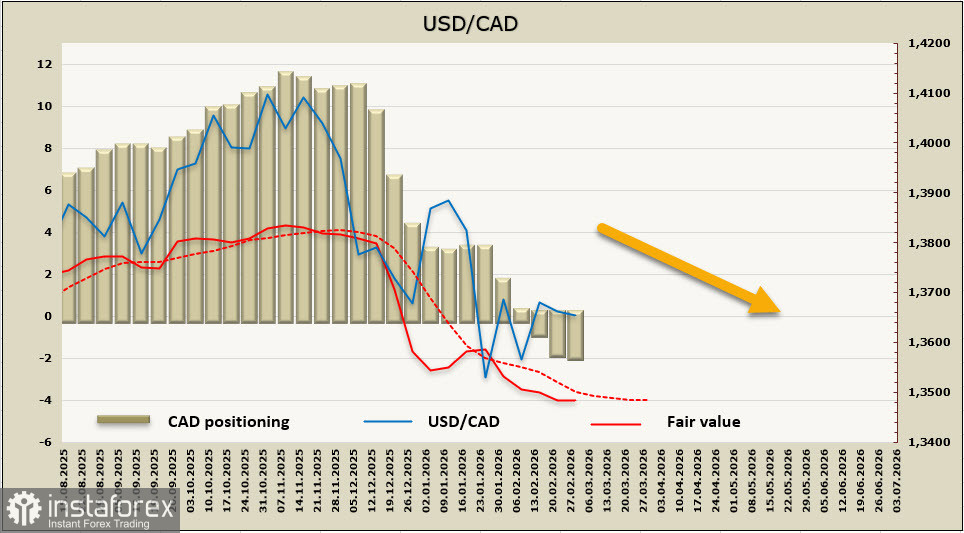

Net speculative long positioning in CAD rose by $119 million over the reporting week to $2.01 billion; positioning is mildly bullish. The implied price remains below the long-term average, but the downward trend has disappeared.

Closure of the Strait of Hormuz pushed oil prices higher and provided support to the Canadian dollar, yet the overall uncertainty has so far prevented commodity currencies from resuming meaningful rallies. USD/CAD has traded in a narrow range and below its trend line since the outbreak of hostilities. In the long run, downside pressure remains in place. We believe a move down to the long-term support at 1.3479 is unlikely in the current environment; trading within a sideways band of 1.3620–1.3750 looks more probable, with a breakout in either direction possible depending on whether the escalation eases or intensifies.