আরও দেখুন

23.06.2026 01:38 PM

23.06.2026 01:38 PM

See also: InstaTrade trading indicators for USDX.

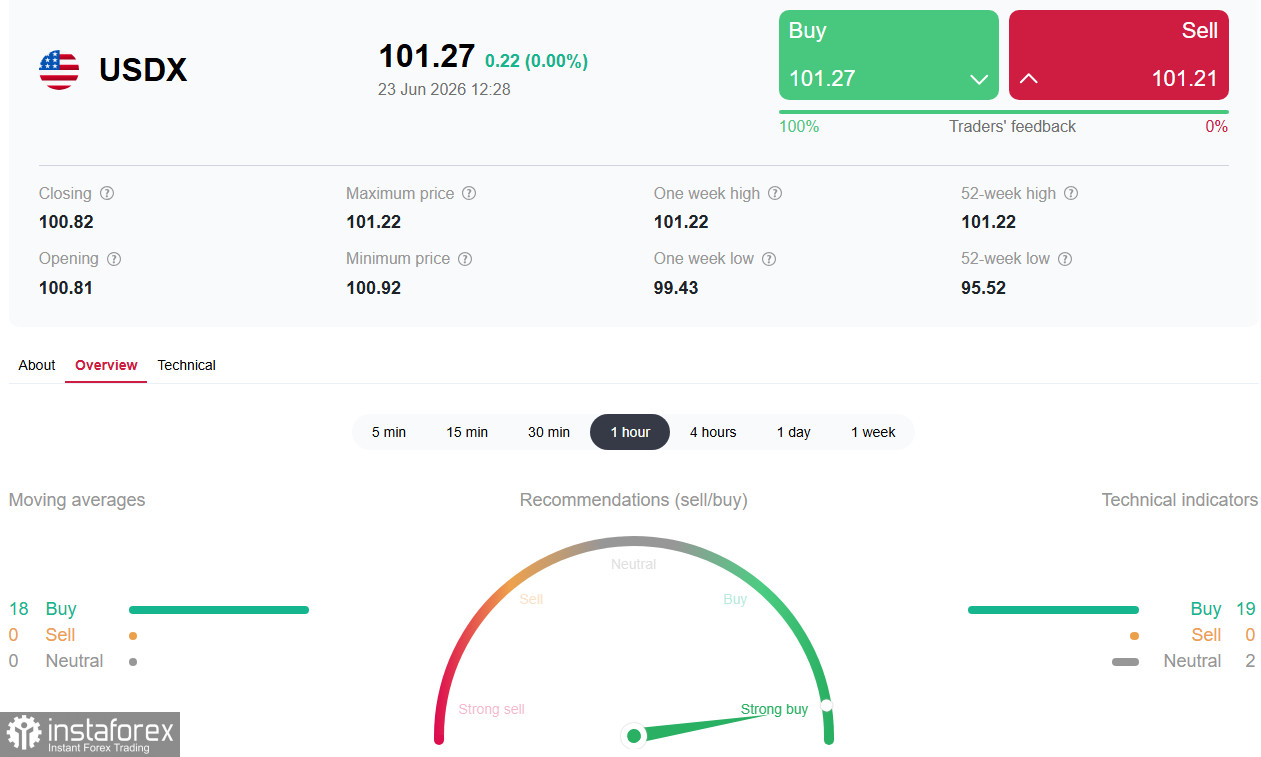

The US dollar index (USDX) continues a confident ascent, holding above the psychologically important 101.00 level during Tuesday trading and consolidating near 13-month highs above 101.20. The principal catalyst for this rally was a hawkish signal from the Federal Reserve and rising expectations of rate increases in 2026.

This week, traders are focused on PMI business activity data and, above all, the Fed's preferred inflation gauge — the personal consumption expenditures (PCE) price index — due on Thursday. Those figures will determine whether the dollar can hold its recent heights or whether a correction will begin.

Fundamental backdrop: Fed's hawkish signal and Warsh's new approach

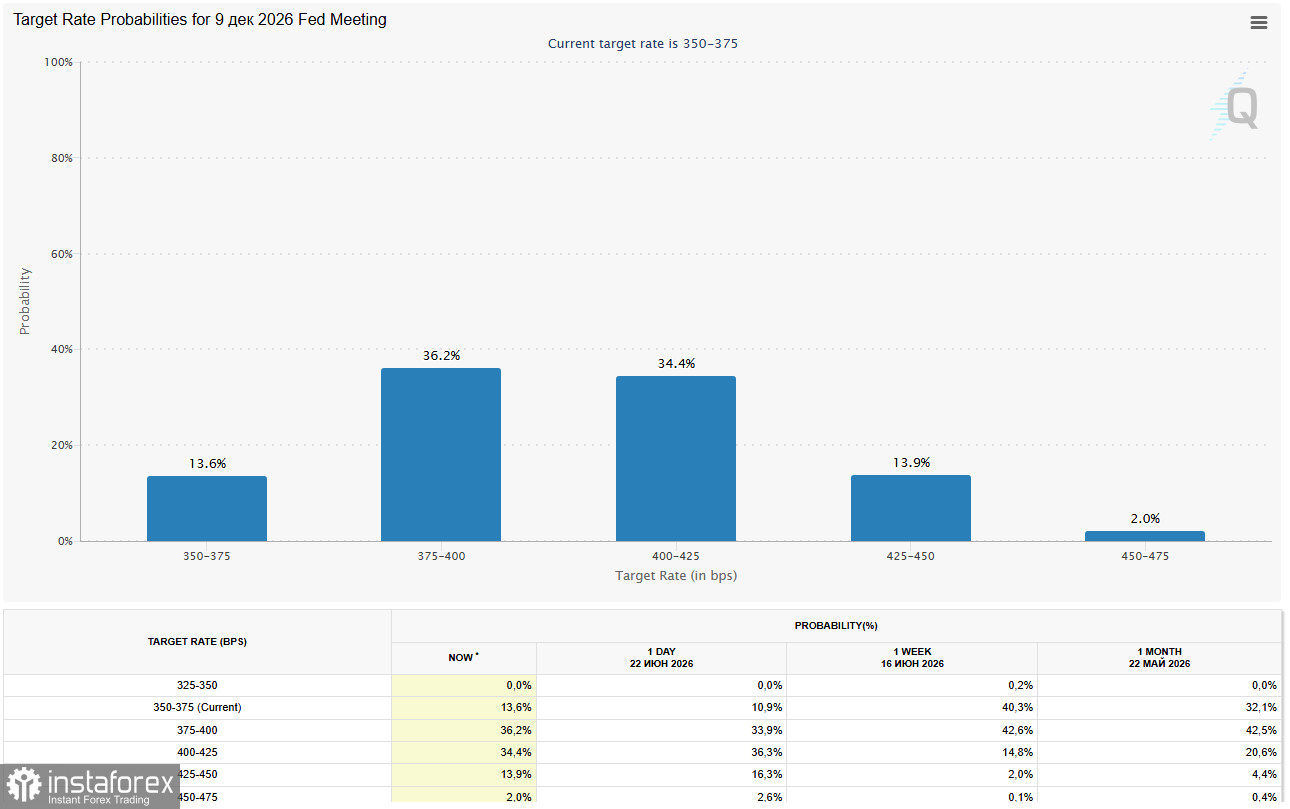

The key driver of dollar strength was the FOMC meeting of 16–17 June. As expected, the Fed left the policy rate unchanged in the 3.50–3.75 percent range, but the first appearance by new Chair Kevin Warsh materially altered market expectations.

1. Dot plot and hawkish signal

The updated dot plot showed a marked shift toward tightening. Whereas in March no FOMC members expected a rate increase in 2026, now nine of 18 policymakers foresee at least one hike, and six of them expect two or more hikes. The median year-end rate forecast was raised to 3.8%, which implies markets have priced an almost 90% probability of a rate rise by year-end.

2. Paradigm shift: end of forward guidance

Kevin Warsh, a frequent critic of forward guidance, has effectively abandoned the practice. The FOMC's accompanying statement was radically shortened and any language implying a policy path was removed. Warsh has said the central bank should be guided strictly by incoming macroeconomic data.

That means markets have lost a familiar anchor and will now react more strongly to each new inflation (PCE), labor market (NFP) and activity (PMI) report. Analysts say this approach "exacerbates volatility and risk premia" because traders must reprice yields in real time.

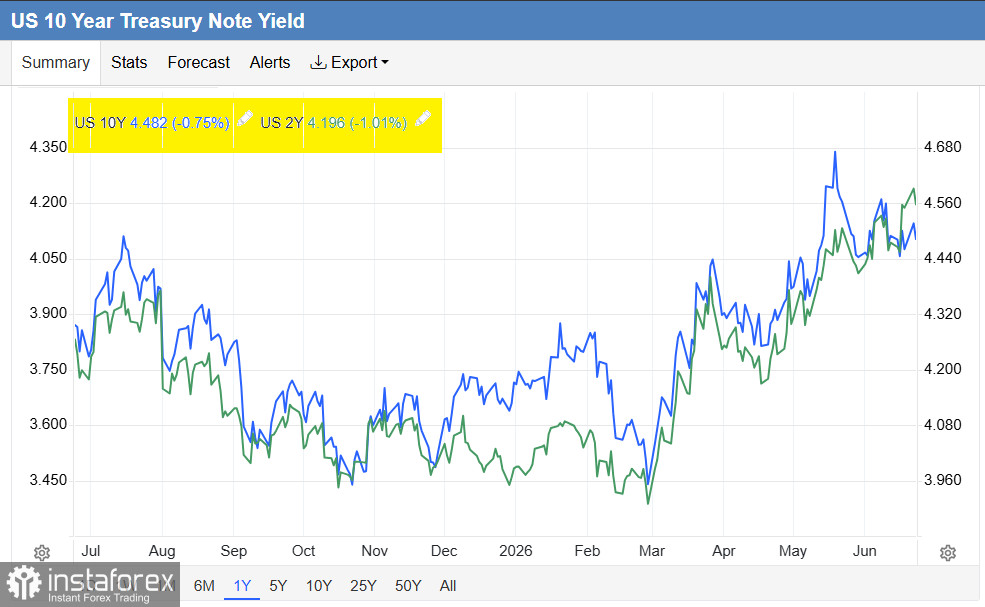

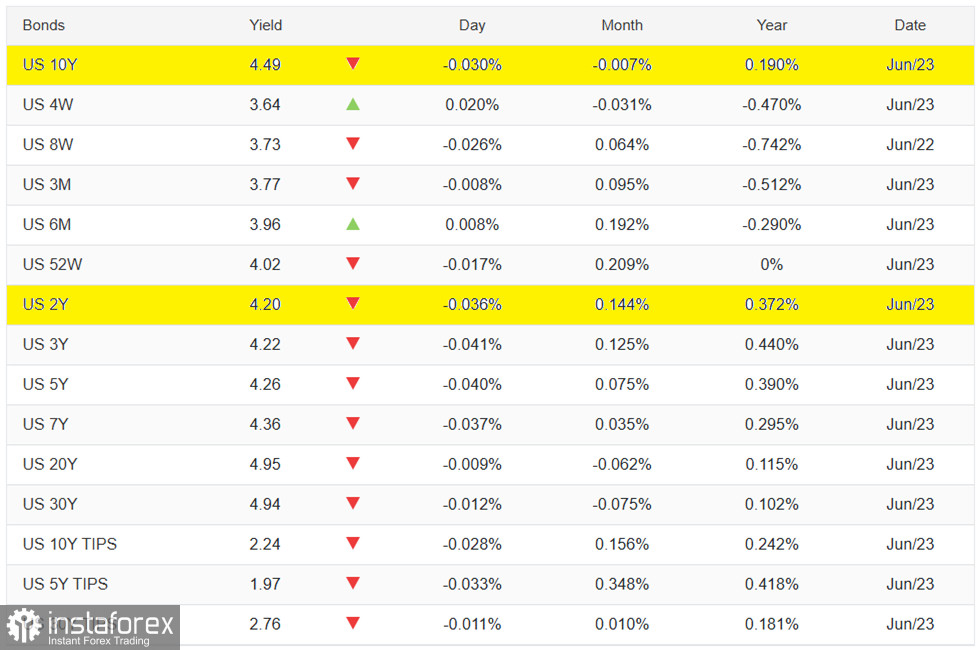

3. Treasury yields and rate differential

Rising tightening expectations triggered a sharp jump in short-term Treasury yields. Two-year yields rose to 4.20 percent, the highest since February 2025. This makes US assets very attractive to global investors amid continued uncertainty in Europe and Asia. The wide interest rate differential in favor of the United States remains the main bullish argument for the dollar.

Macro backdrop: PMI and PCE to test USD

On Tuesday, 23 June, investors will receive preliminary S&P Global PMI data for June. US activity is expected to remain in expansion: the services PMI forecast is 51.0 and the manufacturing PMI 54.8. Stronger-than-expected prints would bolster hawkish expectations and support the dollar; weaker readings would prompt a short-term correction.

The week's main event is Thursday's PCE release, the Fed's preferred inflation gauge. If data show an acceleration in core inflation, that will signal that rate increases are indeed likely, giving the dollar a fresh impulse. Weaker PCE prints could trigger profit-taking and a correction in the dollar from its annual highs.

Brief technical analysis

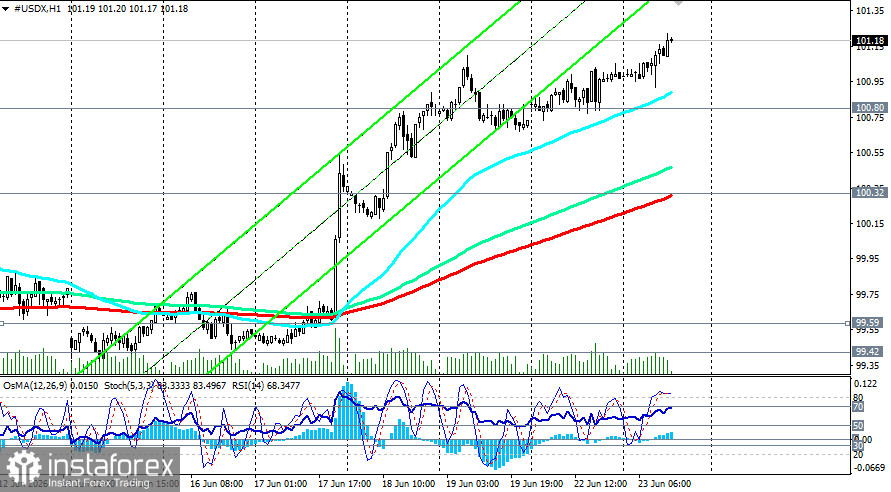

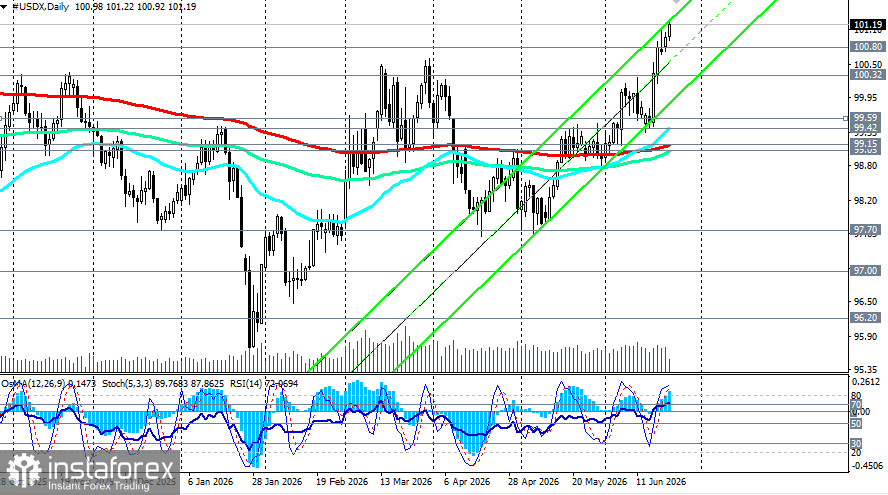

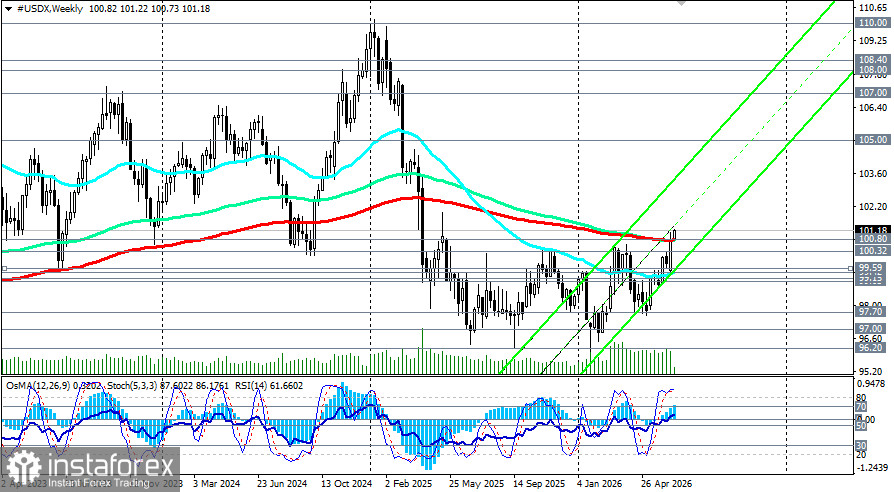

Technically, USDX is in a breakout zone. The index pierced multi-year resistance around 100.80 (the 144- and 200-day EMAs on the weekly chart and the 50-day EMA on the monthly chart) and the psychological 101.00 level, which had served as a key barrier since 2022.

The index trades confidently above 101.00 and is holding above 100.80, which now acts as key support. The short-term bias remains bullish, although the RSI (around 71) has entered overbought territory, suggesting the prospect of short-term consolidation.

Key events to watch (GMT)

| Date(GMT) | Event | Forecast/Expectation | Possible influence on USDX |

| June 23 (13:45) | Preliminary data on S&P Global PMIs (US, June). | Services: 51.0; Manufacturing: 54.8 | Moderate influence: figures above consensus support USD; figures below consensus prompt correction. |

| June 25 (12:30) | US PCE (May). | Core PCE, y/y: 3.4% | Main driver. Figures above consensus may cause fresh USD impulse; figures below consensus may lead to profit-taking. |

| During the week | developments in US-Iran negotiations | — | Escalation may support USD; de-escalation may cause pressure on it. |

Conclusion

The US dollar index is entering a new phase of strengthening driven by a fundamental shift in Fed policy under Kevin Warsh. Abandoning forward guidance, combined with a hawkish dot plot and rising Treasury yields, provides a structural foundation for further dollar appreciation.

Technically, a break of key resistances opens the path to targets of 103.50 (the upper edge of the weekly upchannel) and 105.00. Risks remain - upcoming PCE data may either confirm the hawkish scenario or trigger a pullback from annual highs. In the absence of clear signals from the Fed, markets will be highly sensitive to incoming macroeconomic data.